September 24, 2019

“Tell your parents ‘Don’t worry about the price. It will be worth it. Don’t worry about debt; just accept the (college) offer!’”

Yep, a college sophomore said it with her loud voice during a university “meet and greet” my daughter and I attended this past summer.

Then there was a young woman that financed four years at a prestigious university, is currently living well within her means, and will be done paying off her undergraduate college debt before she is 30 years old.

I now have a young woman in college, and every time I close my eyes to create an image of her, my heart jumps for joy as I reminisce…she is smiling and giggling, barely able to sit up for the first time. However, it is not just the image of her that makes me smile, but the wonderful young woman that she has become. Yet, there is something else: she is ready to manage her own financial assets and take responsibility for her financial decisions. She will make mistakes, because we all do, but I suspect she will be strong enough to make decisions, humble enough to ask for help when she needs it, resilient enough to bounce back from “set-backs”, and focused enough to develop plans to effectively manage her financial life planning goals.

Over the past 5 years or so, I intentionally empowered her to gain understanding about her finances and what it takes to economically function based upon the resources SHE has available to her. Each parent or household has unique processes, however some examples of how I chose to empower my daughter at the onset of her financial life planning journey are listed below.

- At 13 we opened her bank account; she deposited monetary prizes for academic competitions into the account.

- Through Girls Scouts she learned to run a business through Girl Scout product sales programs; she carried a credit card swiper, managed inventory, ran product sales booths, and completed financial statements. She placed her earned monetary incentives into an account for future academic courses and test fees, educational enrichment opportunities, and travel with her Girl Scout troop.

- She was a lifeguard; her pay was directly deposited into her bank account.

- She gained an appreciation for filing and paying taxes.

- As a driver in our household, she was able to use whichever vehicle was available, however she was in a rotation with the other drivers to fill the gas tanks.

- She pays her portion of a roadside assistance insurance policy.

- In the fall of her senior year, we completed the Free Application for Federal Student Aid together.

- Upon graduation from high school, she was required to pay her own cell phone bill; she calculated the cost for an entire year and set aside the amount.

- She was aware of how much college savings and investment funds were available to her and that monetary data point was a relevant factor in her decision-making matrix for her college choice. She set goals for academic scholarships to supplement her college savings accounts and decided if she even wanted to go into debt for certain universities based upon her academic, social, and professional objectives and what a given university offered. That answer was a resounding NO!

- We continue to have conversations about “cost” and “value”, needs versus wants, and the importance of investing in herself and others.

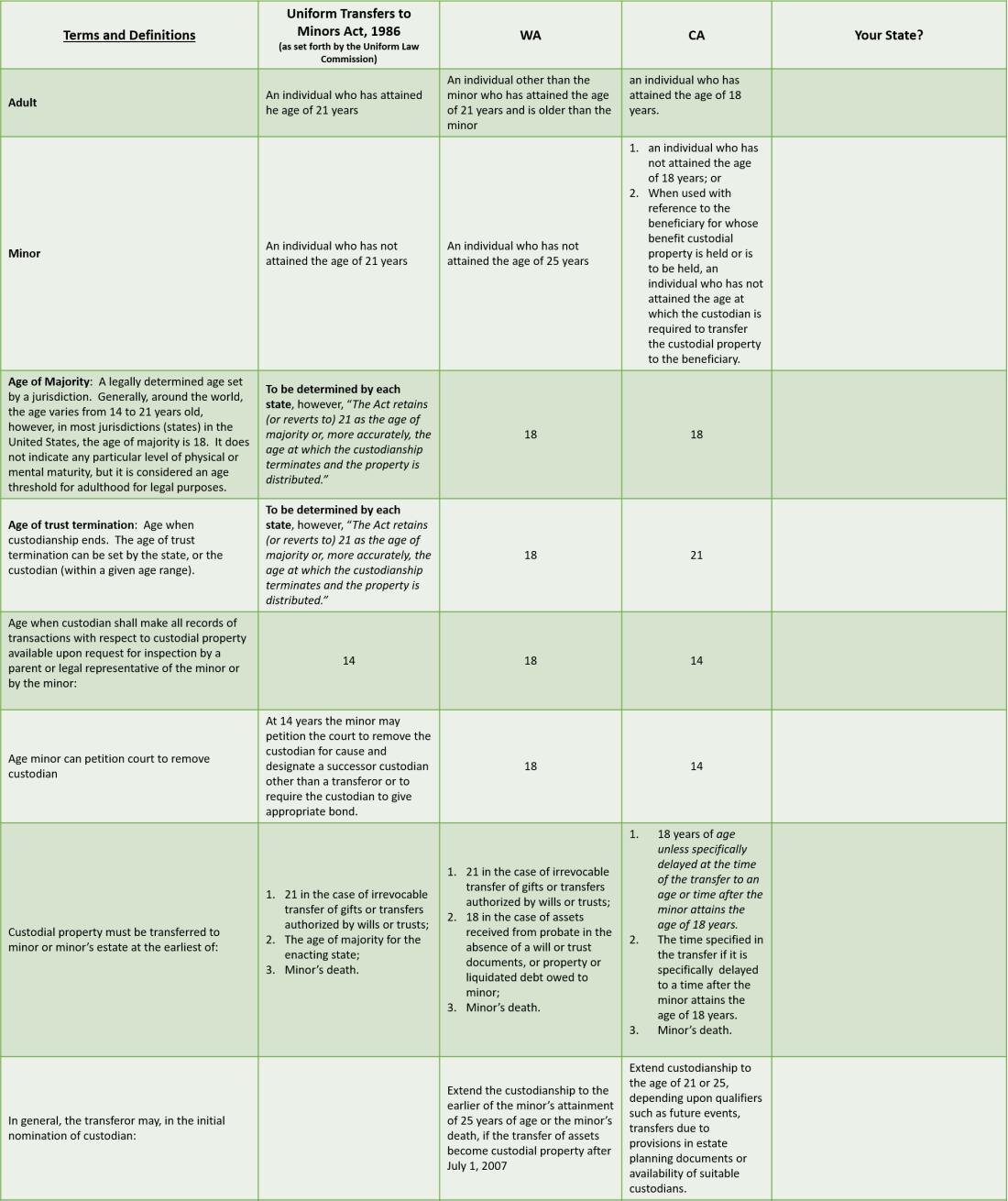

Here’s the thing: With all of my planning, teaching, “monologuing” and saving, I did not intend to turn over her Uniform Transfer to Minors Act assets to her until she turned 21 years old. After all, that is how the accounts were set up soon after she was born. Monies or assets deposited into UTMAs or UGMAs (Uniform Gift to Minors Act accounts) are irrevocable, meaning once the gift is given, the giver (or transferor) cannot reclaim the gift and, until turned over to the recipient, the assets must be used for the benefit of the recipient. Custodians are fiduciaries. However, one of the “selling points” of establishing these savings accounts for minors is that the giver or “transferor” can designate the age at which the recipient receives complete and unfettered access to the assets. Welp, be sure of when you are required to turn those funds over to your young adult and whether or not they are equipped to manage the assets they receive: As a general rule the state of residence dictates when the assets must be accessible to the ultimate owner of UTMA/UGMA assets.

Imagine my surprise when the broker at my investment firm told me that the age of majority (18) in our current state of residence dictates when she gets her money, not where the account was established and how it was titled when established (21)! As we moved around the country and transferred our children’s accounts between brokerage companies, we became subject to a slightly different, yet significant, version of the UTMA state law and the official “titles” of the accounts were inadvertently changed. Well, the truth is that when it comes to the law, we must be aware of circumstances, interpretation, dates, amendments and a host of other factors that are accounted for in the details of the exceptions and substance of each scenario. In addition, brokers do not want to be in the business of giving legal advice. Without the help of trusted advisors, like financial planners and CPAs, clients of brokerage firms will have to do the research to understand the details of transitioning custodial assets to the minor.

Below is a short matrix, which includes some helpful grammar and definitions, to complete for your personal UGMA/UTMA planning purposes. The information should not be construed or relied on as legal or tax advice, but rather a starting point to educate yourself about your UTMA related terms and age restrictions. Seek legal, tax and planning advice before entering into any contractual agreements, opening accounts or executing any financial transactions. There are exceptions based upon varying circumstances, however the information below is meant to be generally applicable. Have a conversation with your high school graduate about when and how the assets will be transferred and any help or guidance you can offer. You may find that he or she wants to establish new accounts with the custodian taking on an alternative role as a power of attorney. Talk to your financial planning professional about what set-up works best for your unique situation. After-all, price is important, college debt is worrisome, and handling personal financial obligations is a sign of good stewardship and integrity.

–Terry